No-fault auto insurance explained: What it means and why it matters

Most drivers know they need car insurance, but fewer understand how it actually works in their state. That's especially true in the states with no-fault insurance. In these states, getting paid after a crash (and whether you can sue) follows a very different set of rules.

No-fault and at-fault systems take two distinct approaches to accident claims. Knowing which one applies affects how quickly you get medical care, recover lost wages, or take legal action.

Learn from Recovery Law Center all about no-fault insurance, how it compares to at-fault systems, and what it means for drivers in different states. Whether you're buying a policy or navigating a recent accident, understanding the rules helps protect your rights and your finances.

What is no-fault auto insurance?

No-fault auto insurance is designed to simplify and speed up claims. After a crash, you don't need to prove who caused it. Each driver files with their own insurer. The goal is fewer lawsuits and faster access to care.

At the center of no-fault coverage is Personal Injury Protection (PIP), which pays for:

- Medical bills. ER visits, rehab, and follow-up care.

- Lost income. Partial wage replacement if you can't work.

- Funeral costs. In fatal crashes, PIP may cover burial expenses.

But PIP doesn't cover everything. It won't pay for car repairs, stolen items, or damage to other vehicles. For that, you'll need collision, comprehensive, or property damage liability insurance.

Some states let you sue if injuries are severe or costs exceed limits. No-fault laws aim to speed up recovery, but they also come with legal trade-offs. Know where the line is in your state.

What is at-fault (tort) auto insurance?

In an at-fault, or tort, system, the driver who caused the crash is financially responsible for the damage, including injuries and property loss. Their insurance pays, as long as they have enough liability coverage.

But before that happens, the fault must be established. That usually involves police reports, witness statements, and damage assessments. Because of this, claims in at-fault states often take longer to resolve.

What do drivers need to carry?

If you're in an at-fault state, your policy usually includes:

- Bodily injury liability. Covers medical expenses for others.

- Property damage liability. Pays for damage to vehicles or properties.

The right to sue

Unlike no-fault states, at-fault systems let you sue right away—even for pain and suffering. That can lead to higher payouts, but it also means more legal costs and longer timelines. At-fault systems offer more legal options, but they also demand a clear answer to one question: Who caused the crash? And that's not always easy to prove.

Key differences between no-fault and at-fault insurance systems

Knowing how these two systems work can make a huge difference when dealing with an accident. Here are the four most significant ways they diverge and why it matters.

1. How claims are handled

No-fault systems prioritize speed. After a crash, each driver turns to their own insurance, with no need to prove who caused the accident upfront. This usually means quicker payouts and fewer lawsuits.

In at-fault states, the opposite is true. Insurers have to figure out who's responsible before paying anything. That means reviewing reports, collecting statements, and sometimes fighting over blame, which can delay compensation.

2. Your right to sue

In no-fault states, your ability to take legal action is limited. You can't sue the other driver unless your injuries are severe or your medical costs pass a certain threshold.

At-fault states give you broader rights. If someone else causes the crash, you can sue immediately, even for minor injuries or property damage.

3. What it costs

No-fault insurance can come with higher premiums since insurers must pay out claims quickly regardless of fault. At-fault systems often reward safe drivers with lower rates over time, but may hit you with rate hikes even for minor mistakes.

4. Who's held accountable

Tort-based systems place clear responsibility on the at-fault driver and their insurer, which can lead to stronger incentives for careful driving. No-fault setups blur that line. Your insurer pays either way, so accountability can feel less direct.

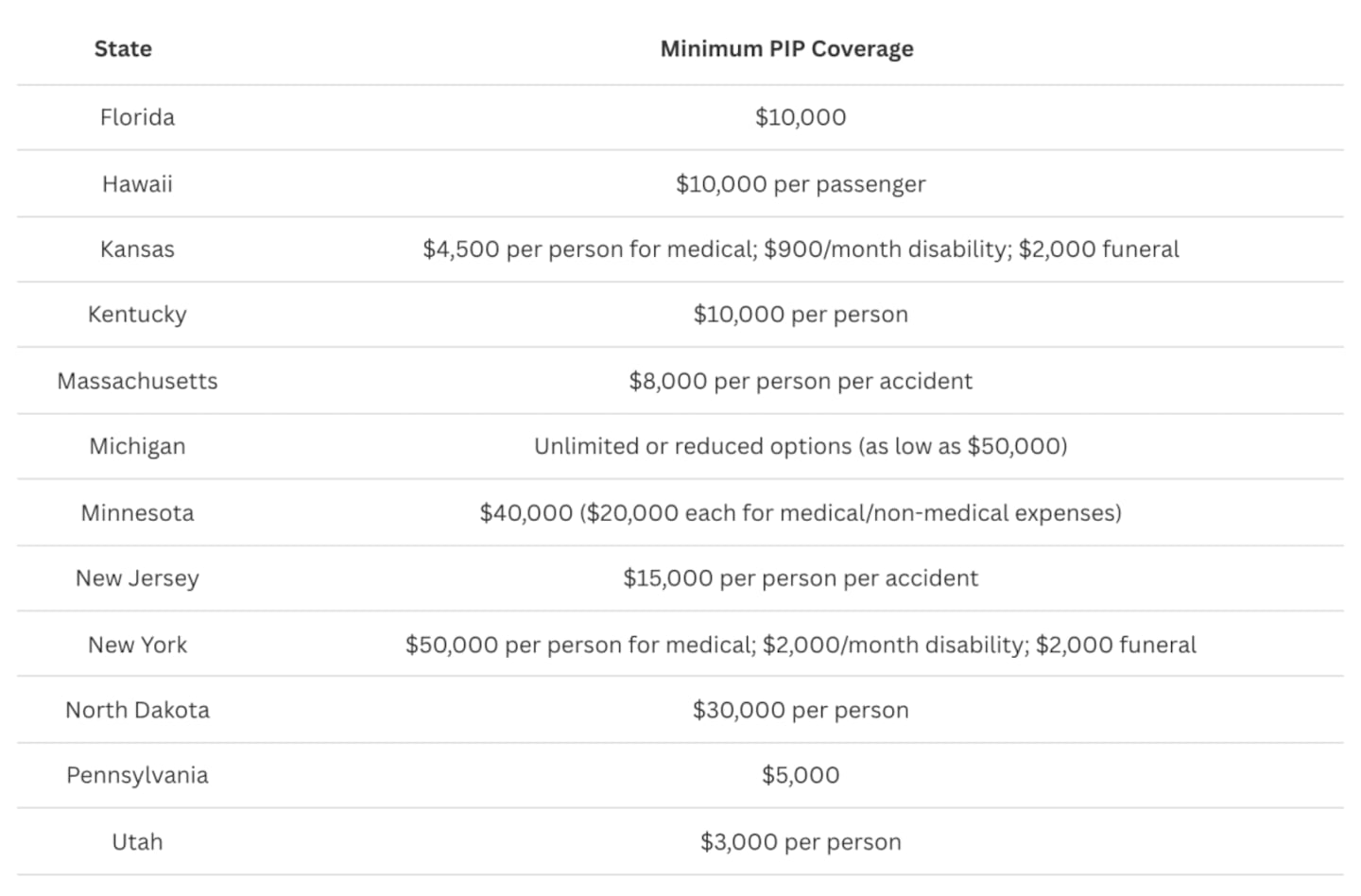

Where no-fault laws apply: The 12 no-fault states

Twelve states in the U.S. use some version of a no-fault auto insurance system. If you live in one of them, you're generally required to carry Personal Injury Protection (PIP) and file injury claims through your own insurer, regardless of who caused the accident.

The core no-fault states:

- Florida

- Hawaii

- Kansas

- Massachusetts

- Michigan

- Minnesota

- New York

- North Dakota

- Utah

The "choice no-fault" states:

- Kentucky, New Jersey, and Pennsylvania give drivers the option to stick with no-fault coverage or opt out and keep full rights to sue under an at-fault model.

Minimum PIP coverage by state

Here's a quick look at what each state requires at a minimum. Some offer stronger protections, while others set fairly low baselines:

Recovery Law Center

Some states, like Michigan and New York, offer more extensive benefits by default. Others, like Utah and Pennsylvania, set lower minimums, making extra coverage a smart option.

Learn your state's rules to help protect your health, finances, and legal rights after a crash. If you live in or drive through one of these states, it's worth reviewing your policy to make sure your coverage fits your needs.

Real-world examples: How no-fault laws shape accident claims

It's one thing to understand no-fault insurance on paper and another to see how it works in real life. These scenarios show how your state's insurance rules can affect everything from how fast you get paid to whether you can sue.

Scenario 1: Minor crash in New York

A driver rear-ends someone at a red light, causing minor whiplash. Since New York is a no-fault state, the injured driver turns to their own insurer and files a PIP claim. Medical bills and lost wages are covered quickly, and there is no need to prove fault.

But here's the catch. They can't sue the other driver for pain and suffering unless their injury meets New York's strict "serious injury" standard. That includes things like permanent loss of use, significant disfigurement, or a major disability.

Scenario 2: Severe accident in Michigan

A high-speed crash sends a driver to the hospital for weeks. Michigan's no-fault system steps in immediately, and thanks to its unlimited PIP option, all medical expenses are covered, regardless of who caused the crash.

If the injured person wants to sue for pain and suffering, though, they still need to meet Michigan's threshold for serious impairment of body function. It's not always easy to prove, but the strong PIP benefits ease the financial pressure in the meantime.

Scenario 3: At-fault collision in Texas

Two cars collide at an intersection, and one driver is clearly to blame. In Texas, which follows a traditional at-fault system, the injured party files a claim against the other driver's insurance.

That claim kicks off a process that involves fault investigation, insurance adjusters, and maybe even court. The upside is that the injured driver can pursue broader damages, including pain and suffering, from day one. The downside? It often takes longer, especially if the claim is disputed.

Notable state variations in no-fault insurance

While all no-fault states share some basic rules, each handles coverage and legal thresholds a little differently. Here's how four key states stand out:

Florida: Limited right to sue

Florida requires drivers to carry at least $10,000 in PIP coverage, which helps cover medical costs quickly. But suing the at-fault driver isn't easy. To pursue pain and suffering, your injury must be permanent, significant, or involve scarring or disfigurement.

Michigan: Generous benefits, high costs

Michigan lets drivers choose their level of PIP coverage, from $50,000 to unlimited. This offers some of the most comprehensive protection in the country, but it also drives up premiums. Recent reforms aim to bring those costs down while preserving consumer choice.

New York: High PIP, strict injury rules

New York's system requires a minimum of $50,000 in PIP coverage, covering both medical expenses and lost wages. But if you want to sue for non-economic damages, your injuries must qualify as serious (think permanent loss of use or significant disfigurement).

Hawaii: Low threshold, tight restrictions

Hawaii mandates just $10,000 in PIP coverage and follows a more restrictive no-fault model. Lawsuits are only allowed when injuries involve over $5,000 in medical costs or result in permanent damage. This keeps lawsuits down, but can also cap your compensation.

Each no-fault state strikes its own balance between quick payouts and legal limits. If you live in one, it's worth understanding the fine print, especially before an accident puts your coverage to the test.

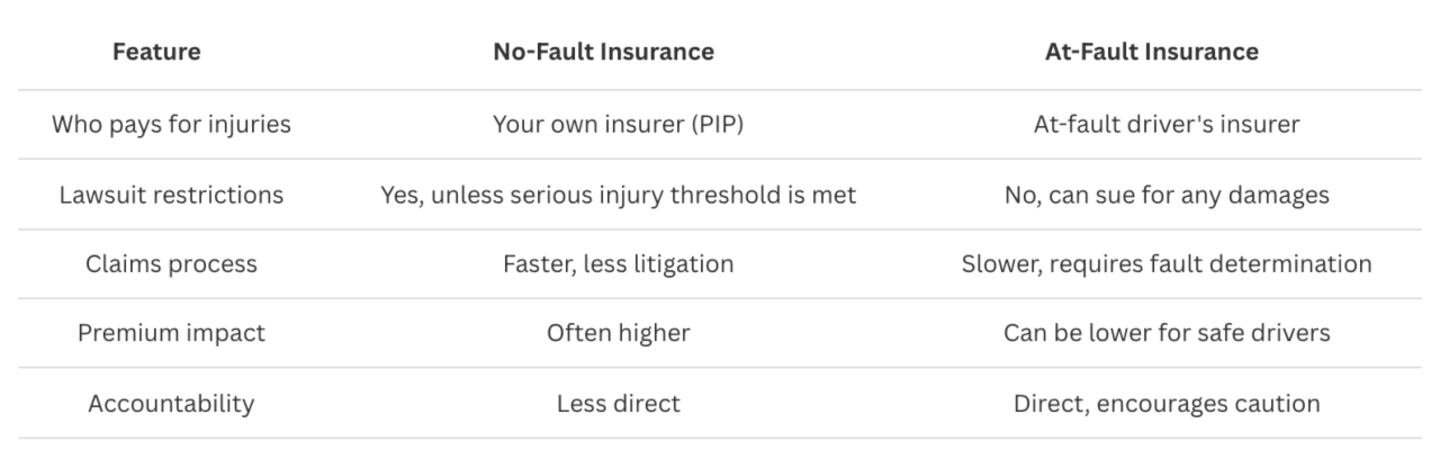

Side-by-side: How no-fault and at-fault insurance compare

No-fault and at-fault insurance systems shape what happens after a crash, like how fast you're paid, who pays, and whether you can sue. Here's how they differ across key areas:

Recovery Law Center

Know the system before you need it

The type of insurance system your state follows shapes everything after a crash. From how fast you get paid to whether you can sue, it directly affects your recovery and legal rights. If you're in a no-fault state, expect limits on lawsuits and faster access to medical coverage. In at-fault states, you may have more freedom to seek compensation, but often with more delays and legal steps.

Either way, it pays to know the rules. Take a few minutes to review your policy and confirm your state's requirements through your Department of Insurance website. That one small step now could save you a lot of time, money, and stress when it matters most.

This story was produced by Recovery Law Center and reviewed and distributed by Stacker.

Sign Up

Sign Up